Are you accessing Australia’s lowest taxation rate, making the most of your concessional contributions and non-concessional contributions into your superannuation?

Habitus Wealth Creation will help you understand the benefits of additional superannuation contributions. We will invest time to understand your short and long term goals, then develop a superannuation strategy that suits your lifestyle and reduces the tax you pay.

Our tailored advice will explain:

- * Concessional contributions and non-concessional contributions, helping you maximise the tax benefits including salary sacrifice.

- * Different levels of investment types within superannuation.

- * SMSF (Self Managed Super Funds)

Changes to Superannuation – 2017 – Plan ahead to maximise your super!

The Australian Taxation Office (ATO) plan to introduce significant change to both concessional contributions and non-concessional contributions, which are likely to take effect in July 2017.

The changes that will have the biggest impact for most Australians are:

- * Reducing the concessional contributions cap to $25,000 for all taxpayers.

- * Reducing the non-concessional contribution cap to $100,000 pa (or $300,000 under the bring forward provisions), limiting the ability to make non-concessional contributions (NCCs) to people who have a total superannuation balance of less than $1.6 million and introducing transitional rules for those who triggered the bring forward rule prior to 1 July 2017.

- * Introducing a $1.6 million transfer balance cap, which limits the amount that can be transferred to the retirement phase, where earnings are tax-free. This measure will also apply to death benefit income streams.

- * Increasing the annual income threshold from $10,800 to $37,000 for eligibility for the spouse contribution tax offset.

Today, Salary Sacrifice (before tax) is one of the most tax effective ways to build wealth in your super, as these concessional contributions are taxed at only 15%. The higher your marginal tax rate, the greater the benefit. These changes may also provide before tax and after tax opportunities for spouse contributions, further growing your long-term super, so planning ahead is critical.

Our clients are surprised at the minimal impact salary sacrifice concessional contributions have on their take home salary; it’s a simple case of smarter investing to build your wealth.

Speak to us today and we will help you better understand the changes and ensure you plan ahead to take advantage of the current and future rules relating to concessional contributions and non-concessional contributions in superannuation.

Case Study One – Concessional contributions – Doubling your super contributions, without the large personal sacrifice!

We have all heard the stories about the high percentage of Australians who will not receive enough annual income from their super for retirement and those that did not take advantage of concessional contributions. In fact the annual short fall for males can be as high as $8,722 per annum or females 15,031 per annum (Industry Super Australia’s Findings 4 June 2015).

For the smart investor, that does not necessarily need to be the case. Your employer is obligated to contribute 9.5% of your salary into super, so if you are earning $100,000 per annum, that’s $9500 or $8075 after the 15% super contribution tax. If you were to salary sacrifice the same amount imagine the difference that would make to your annual income in retirement. You could achieve this without the huge personal sacrifice. Breaking it down, it could mean a net difference to your take home pay of only $111.44 per week. For most people earning $100,000 per annum, that’s very achievable. Best of all the $111.44 you sacrifice, provides you with $155.29 in your super, as a result of the tax benefits. Naturally this would be subject to your overall tax obligations and deductions, which varies from person to person. If you really think about it, the small salary sacrifice basically doubles your annual super contributions and could mean a significant difference in the life you lead in retirement. That’s plain and simple, smarter investing.

Let’s take Sally, who is 39 years of age and earning $100,000 per annum. The table on the left, is a breakdown of her take home pay without any salary sacrifice and the table on the right is her take home pay after salary sacrifice. You will see the difference in her annual net income is $5,795 or $111.44 weekly and the additional net contribution to her super is $8075 or $155.29 weekly. Just think about that, she is sacrificing $111.44 to add $155.29 to her super, so she’s 39% better off. I call that a very good return on investment without additional risk.

As everyone’s situation is different, we recommend you contact us and we can walk you through the different scenarios that would be right for you. Let us help you to become a smarter investor for retirement by making the most of concessional contributions.

Case Study Two – Leveraging the tax benefits, with Non-Concessional Contributions

Life can be quite ironic. We spend a lot of time thinking about the car we are about to purchase or the new shirt or dress for that special occasion, however we do not give a lot of thought to how we should be investing our hard earned money. Have you ever thought about the difference between investing inside or outside your super and making the most of non-concessional contributions? The tax benefits are substantial. For starter’s any interest you earn outside super is subject to standard tax rates, so for someone earning $100K pa, that could be as high as 39% vs a low 15% if you had the funds invested into your super. Just think about that for a moment that’s a difference of 24% per annum. If you start to think about the compound effect year-on-year, it’s a significant difference.

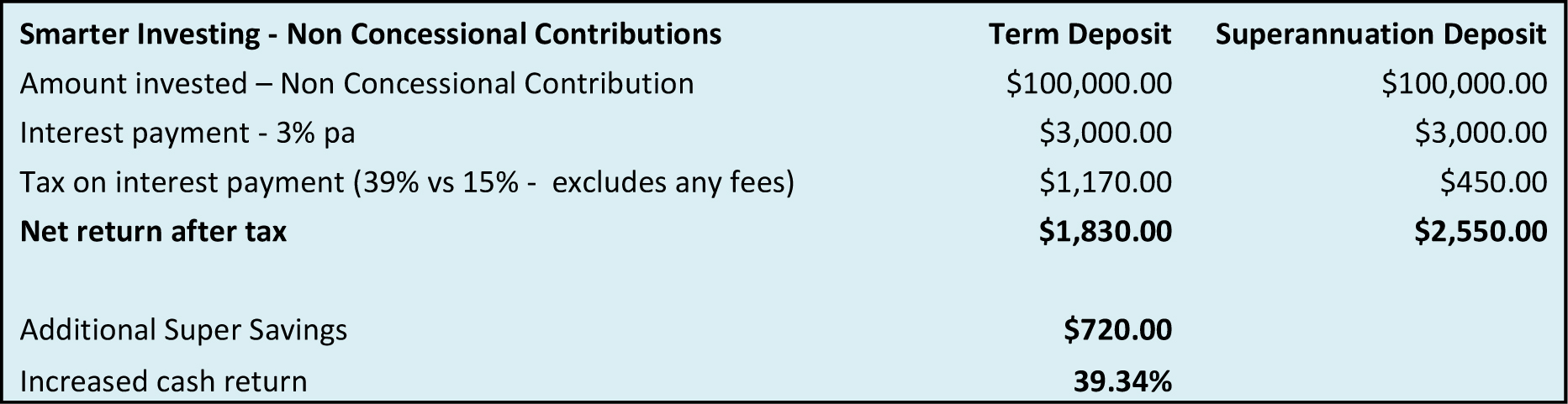

Let’s take John who has $100K invested in a 12 month term deposit. As John is earning $100K per annum, the interest he earns on his term deposit is subject to standard tax rates, in his case 39% (37% tax and 2% Medicare levy). As it’s a term deposit, he is only getting a return of 3%, which equates to $3,000 per annum in interest. He then has to pay $1170 in tax, leaving him a net return of only $1830. If he had invested into his super at the same rate of return, he would be paying only $450 in tax, leaving him a net return of $2550. That’s an additional $720. By making a non-concessional contribution to his super, John has increased his cash return by 39.34%. Imagine the benefit over the long term and the difference that would make to the level of living when he retires (all things being equal).

In the table below you can see these calculations broken down. The left column is the return in a term deposit and the right column is the return within super. $1830 vs $2550 respectively providing an increase cash return of 39.34% in 12 months.

Naturally everyone’s situation is different, so speak to the team at Habitus Wealth Creation and we will help you to better understand the various options for smarter investing with non-concessional contributions in super.